Tango.vc Fund Performance

I’m sharing a recent LP update, including our outlier fund metrics.

I just sent out an update to Tango LPs, and here is a (slightly modified) public version.

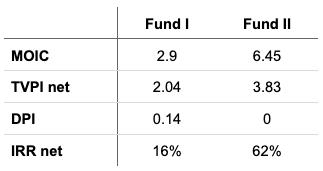

Performance

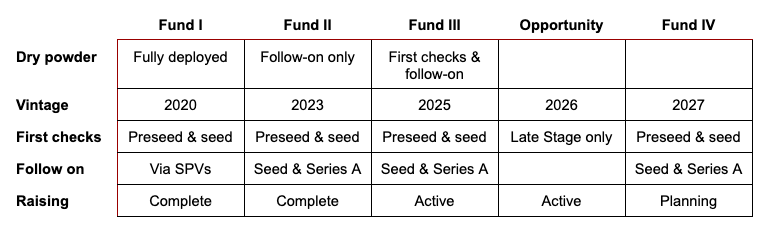

Fund I and Fund II are closed, and we’re in the marketing period for Fund III, at the tail end of the raise. We’ve made some investments out of Fund III, but haven’t started reporting on metrics yet. See the section below about how we mark value.

Fund I also had 3 SPV follow on investments, and one was in the current leading company, Hydra Host, which makes software for datacenters. That SPV is sitting at 18X gross, which after 4 years means over 100% gross deal IRR. We used SPVs rather than reserves in Fund I for follow-on. If you combine them, Fund I is 2.2 TVPI net and 18.2% net IRR.

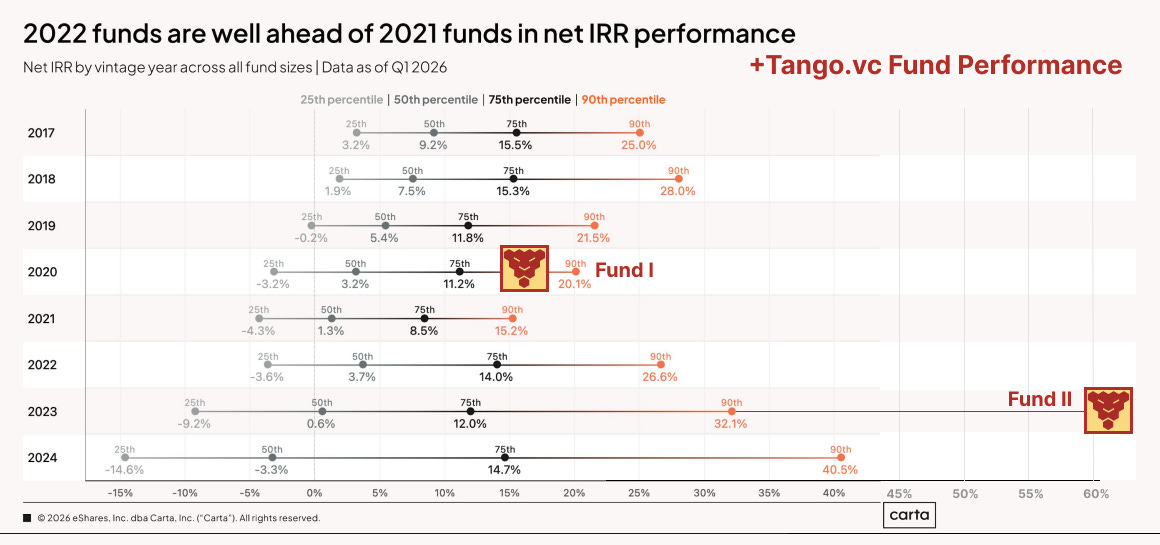

Carta provides useful comparison reports on fund performance by vintage year. Find the latest here. I took their report on net IRR percentiles by vintage year, and literally needed to extend the chart to show how we compare. Fund I was 2020, and Fund II was 2023. Fund I is around 80th percentile, and Fund II is an outlier far above 90th percentile, literally off the chart to the right.

Announcing the Tango Opportunity Fund

We’re seed and preseed investors, but we’ve been successful enough that our portfolio companies are now at a later stage. We’re announcing the first Tango Opportunity Fund! We’ll invest in the late stages of companies we back in the seed and preseed. This is an excellent opportunity for LPs to get access to companies. It’ll be concentrated, with 8-12 investments, focused on late stage rounds from clear winners, and an average of $5M per investment.

The math of later stage investing means we can’t manage this with reserves from the fund. The minimum investment in very large rounds would make the seed fund reserves too concentrated. Normally we’d invest in 25 to 40 first checks and then follow on in at least 8-12. Read more about concentration math in this post, and read below to get a sense of the rounds, like the full Stoke Space Series D at $860M.

There are two advantages for investors in the Opportunity Fund:

We’ve tracked the company from the beginning learning what makes them great.

We earn access by building great relationships with founders.

This will also generate early liquidity for our seed funds in some cases. When we’d like to invest in late stage rounds but can’t because they are dramatically oversubscribed, we’ll consider an affiliate transfer from the seed fund to the opportunity fund. Because we’re managing both sides, it’s important to be clear upfront on how pricing works. It’s only possible with a coincident priced round to make the pricing objective. There are also rules that limit the share of VC fund secondaries, so this would be at most 20% of the fund. We’d also want to keep upside for seed fund LPs, so the rule of thumb is selling a minority of a stake for a substantial return.

For example, our Fund II stake in Lovable is such that we can sell a minority position and more than 2X the whole fund. Over 60% net IRR is an exceptional state for a fund to be in, but a lightning fast 2X DPI is ridiculous. It’s also worth mentioning that my GP interest here is actually neutral, getting carry from either fund. So it’s all about what is best for LPs.

We’re at the tail end of the raise for Fund III, currently in the marketing period. We’ll start the Fund IV raise after that, with a target first close in 2027. That means there are a few vehicles in the air, and to clarify, you can see a table below.

If you’re interested in learning more email ivan@tango.vc

Robotics & Hard Tech Rising

I just reviewed all the companies in the spring batch for YC, and it’s notable how many companies are in hard tech and robotics. For a while, this wasn’t the trend, with SaaS and crypto dominating.

Here are a few speculative reasons for this:

Founders fear software won’t have a moat.

Higher performance on the perception and controls for robotics.

Giant companies like Tesla and SpaceX demonstrated immense value at scale. This influences both founders and investors.

Those companies trained thousands of next generation founders.

I think it’s an incredibly good time to back the companies we’ve been focused on since the beginning. It’s also worth reflecting on how consistently wonderful YC has been for the whole startup community.

Portfolio News

Stoke Space extends Series D

They had announced a mega financing, and now it’s even bigger, going from $510M to $860M raised. I’m writing this as SpaceX IPOs, as one of the largest IPOs ever. The largest space launch company is valued at $2T. As a reminder, Falcon 9 crashes every single second stage on its maiden voyage, and Starship is all about fixing this with a reusable second stage. Starship is still in development, and Stoke Space is in the same race for full and rapid reusability. Stoke is one of our best investments in Tango Fund I, now worth 15X. Stoke valued at 1% of SpaceX would 3X Fund I.

Coram raised a Series B

Read more about the news here. They build site security systems that include intelligence surveillance video processing, like being able to search video with natural language “find the guy in the blue hoodie”. I just visited with founder Ashesh Jain who impressed me with their work – especially around AI. It’s becoming clear that some companies are embracing the changes and applying them everywhere. Engineers can own a whole product from idea to building to business impact. Tools change too: for example Ashesh said “a CRM is really just a stack of APIs that are used by our agents and processes”.

Hydra Host announced their Series A

Read more about it here. We reported on the round in the last update, but they completed the financing and just announced it. Hydra makes software for datacenters, and with the AI datacenter buildout, they’ve grown really fast. This is the top performing investment so far in Fund I, and we also made an SPV follow on investment that is doing well.

Ultra Robotics publicly launched.

You can read more here. It’s notable as a contrast from humanoids because it has arms but is fixed with no legs or batteries. One trend I’m tracking is companies that use models to do their work. There is an immense amount to solve for customers that is outside the core behavioral models. This is like pre-ChatGPT era of models, and I think investing in both robotics foundation models and new robotics businesses that build on top of them is viable.

How to Mark Value

It’s worth revisiting some guidelines I put on how to value companies. I think the most objective metric is priced rounds and complete company actions like acquisitions or wind downs. I’ve thought about incorporating other signals, but my previous experience shows this is fraught.

What happens if a company raises a bridge on a high cap SAFE? Presumably the next round will be close to that cap, and this should be higher value. But what if that round never comes? Alternatively, let’s say I haven’t heard from a company in a while, with no investor updates. Should I mark that down? A few times, the first I’ve heard of a company in a while is a new priced round. Founders were just heads down building.

When times are flush, you can raise money easily, and some disciplined founders use that to extend the time they have to figure it all out. After some tightening a few years back, money is loose and the seed rounds of today can be made to last a long time.

Really appreciate the clarity and depth of your update! But I'm not surprised - it's par for the course.

To anyone reading this: Whether you are a founder or LP, you should jump at the chance to work with Ivan. He's the real deal.

Love the update! Ivan and Tango have been amazing to work with, if you're considering Tango, I wouldn't hesitate.